You know the scenario. A new client sits down for their first planning meeting, hands you a crumpled bank statement from three months ago, and says "I think I have a 401(k) somewhere." Now you're spending the next two weeks chasing account numbers, insurance policies, and tax returns instead of doing what you were hired to do — building a financial plan.

A comprehensive financial planning questionnaire fixes this. Send it before the first meeting, and you walk in with a clear picture of the client's assets, liabilities, goals, and risk tolerance. Below you'll find a ready-to-use template with 38 questions organized by category, variations for four common client types, and a faster way to collect completed questionnaires and supporting documents without the email back-and-forth.

What Is a Financial Planning Questionnaire?

A financial planning questionnaire is a structured form clients complete before their first meeting with you. It captures the personal, financial, and lifestyle information you need to build a comprehensive plan — from household income and existing investments to retirement timelines and estate planning wishes.

A well-designed questionnaire typically covers:

- Personal and family details — names, ages, dependents, marital status

- Income and employment — salary, bonuses, business income, side revenue

- Assets and liabilities — what they own, what they owe, and to whom

- Insurance coverage — existing policies and gaps

- Goals and priorities — retirement age, education funding, major purchases, legacy planning

Think of it as the intake form a doctor uses before an exam. You wouldn't prescribe treatment without a full medical history. Financial planning works the same way — you need the complete picture before you can recommend a strategy.

Financial Planning Questionnaire Template

These 38 questions cover every area of a comprehensive financial plan. Adapt them to your practice — some advisors combine sections, others split them into shorter forms sent at different stages of the engagement.

Personal & Family Information

- Full legal name — as it appears on tax returns and legal documents.

- Date of birth — needed for retirement projections, Social Security estimates, and age-based account rules.

- Marital status — single, married, divorced, widowed. If divorced, note any alimony or child support obligations.

- Spouse or partner's full name and date of birth — needed for joint planning, beneficiary designations, and Social Security spousal benefits.

- Dependents — names, ages, and relationship (children, aging parents, others). Include any dependents with special needs.

- Home address and phone number — primary contact information.

- Preferred communication method — email, phone, text, or video call.

Income & Employment

- Current employer and job title — for both client and spouse, if applicable.

- Annual gross income — base salary, bonuses, commissions. Break out each component.

- Spouse or partner's annual gross income — same breakdown.

- Other income sources — rental income, business income, Social Security, pensions, alimony, dividends, side businesses.

- Employer benefits — 401(k) match percentage, stock options, RSUs, pension, deferred compensation, HSA contributions.

- Expected income changes — upcoming raise, career change, planned retirement, sabbatical, or reduction in hours.

Assets & Investments

- Cash and savings — checking, savings, money market funds, CDs. Include approximate balances.

- Retirement accounts — 401(k), 403(b), IRA, Roth IRA, SEP IRA, SIMPLE IRA, pension. List each with custodian and approximate balance.

- Taxable investment accounts — brokerage accounts, stocks, bonds, mutual funds, ETFs.

- Real estate — primary residence, rental properties, vacation homes. Include estimated market value and outstanding mortgage balance.

- Business interests — ownership stakes, estimated value, and percentage owned.

- Other assets — stock options, RSUs, crypto, collectibles, trust assets, expected inheritances.

Liabilities & Debts

- Mortgage(s) — lender, outstanding balance, interest rate, monthly payment, remaining term.

- Student loans — balance, interest rate, repayment plan type (standard, income-driven, PSLF-eligible).

- Auto loans — balance and monthly payment for each vehicle.

- Credit card debt — total balance across all cards and average interest rate.

- Other liabilities — personal loans, HELOCs, medical debt, family loans, business debt with personal guarantees.

Insurance Coverage

- Life insurance — type (term or permanent), death benefit, annual premium, carrier. List each policy for both spouses. (For a deeper dive on life insurance intake questions, see our template for agents.)

- Health insurance — employer or individual, plan type, monthly premium, deductible, HSA or FSA balances.

- Disability insurance — short-term, long-term, or both. Coverage amount and elimination period.

- Long-term care insurance — do you have a policy? If not, is this something you've considered?

- Property and casualty insurance — homeowner's, auto, umbrella liability. Note coverage limits.

Retirement Goals

- Target retirement age — for both client and spouse.

- Desired retirement lifestyle — maintain current living standard, downsize, travel, relocate. Help the client put a number on it.

- Estimated monthly retirement expenses — or a percentage of current income they'd like to replace.

- Social Security strategy — have you reviewed your Social Security statement? When do you plan to begin benefits?

Risk Tolerance & Risk Profile Questions

- Risk tolerance self-assessment — if your portfolio dropped 20% in a single quarter, would you sell, hold, or buy more? (Conservative / Moderate / Aggressive)

- Investment experience — how long have you been investing? What types of investments have you held? Any past experiences that shape your current views?

- Investment preferences or restrictions — ESG/socially responsible investing, sector exclusions, religious-based guidelines, no individual stocks.

Estate Planning & Tax Situation

- Existing estate documents — will, revocable trust, power of attorney, healthcare directive? When last updated? Who is your estate attorney?

- Tax filing status and bracket — filing status, approximate federal and state bracket, ongoing tax issues (audits, back taxes, estimated payments). Are you working with a CPA?

Questionnaire Variations by Client Type

The 38 questions above cover the fundamentals, but not every client needs the same emphasis. Here is how to adjust for four common client types.

Young Professionals (Ages 25-35)

This group usually has more liabilities than assets. The conversation centers on cash flow, debt payoff strategy, and building an emergency fund. Add questions about student loan forgiveness eligibility, employer vesting schedules, and whether they're maximizing their 401(k) match. Skip estate planning for single clients without children, but always ask about beneficiary designations — you'll be surprised how many 30-year-olds still have a parent listed from the account they opened at 22.

Pre-Retirees (Ages 55-65)

The timeline is short and the stakes are high. Add questions about Social Security optimization (claim at 62, full retirement age, or 70?), Medicare enrollment timing, catch-up contributions, and Roth conversion windows. Include pension payout options — lump sum vs. annuity — since this is often the single largest financial decision a pre-retiree will make. Expand estate planning to cover trust structures, beneficiary designations, and charitable giving strategies.

Business Owners

Business owners blur the line between personal and business finances, and missing that overlap can derail a plan. Add questions about business structure (LLC, S-corp, C-corp), valuation, buy-sell agreements, key person insurance, and succession planning. Ask whether they're funding retirement through the business (SEP IRA, Solo 401(k), defined benefit plan) and whether business debt carries personal guarantees. Business owners almost always underinsure on disability — make it a priority section.

High-Net-Worth Clients ($1M+ investable assets)

Complexity compounds at every level. Expand questions on estate and gift tax planning, generation-skipping trusts, donor-advised funds, and philanthropic goals. Add questions about concentrated stock positions, alternative investments (private equity, real estate syndications, hedge funds), and tax-loss harvesting. Ask about multi-state tax obligations if they own property across state lines. These clients typically work with a team — ask who else is involved (CPA, estate attorney, insurance specialist) so you can coordinate rather than duplicate.

Financial Planning Questionnaire vs. Fact Finder

Advisors use both terms, often interchangeably, but they aren't quite the same document. A fact finder is the compliance-driven form: the structured record of hard numbers your broker-dealer or regulator expects on file, covering income, assets, liabilities, insurance policies, and beneficiary designations. Many firms inherit a standard fact finder template from their custodian or compliance department.

A financial planning questionnaire is broader. It captures the same financial data but adds the discovery questions a fact finder leaves out: goals, priorities, risk attitudes, family circumstances, and how the client actually feels about money. It's a planning tool first and a record-keeping tool second.

In practice, the template on this page works as both. If your firm already has a mandated fact finder, use the sections above to fill its gaps (particularly the goals, risk profile, and estate planning questions) rather than asking clients to complete two overlapping forms.

How to Collect Completed Questionnaires and Financial Documents

The questionnaire is only half the job. You also need supporting documents — two years of tax returns, investment statements, insurance declarations, estate documents, Social Security statements. Sending the questionnaire by email and chasing documents in a separate thread creates two to three weeks of back-and-forth before you can start the plan.

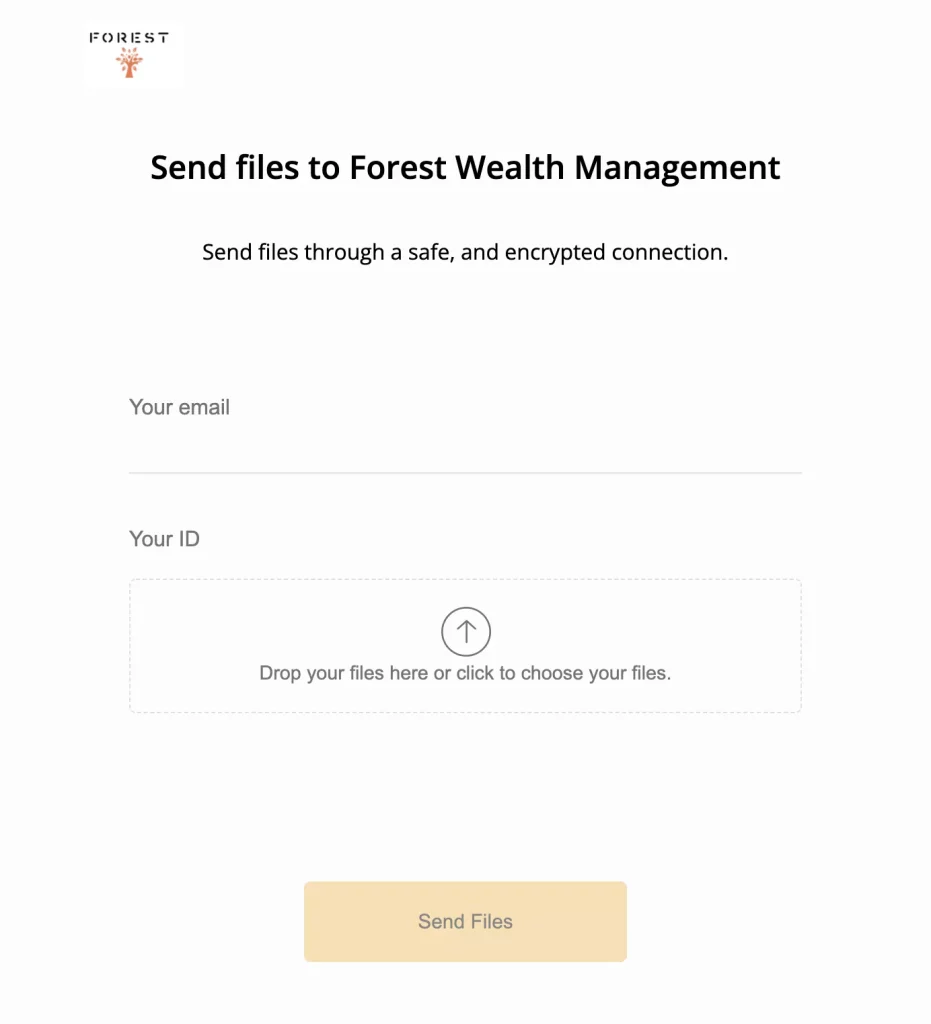

File Request Pro lets you collect questionnaire responses and supporting documents in one submission. You build a branded upload page with form fields for questionnaire answers and file upload slots for every document you need. The client opens a link — no login, no account creation — fills in their answers, drags in their files, and hits submit. Everything lands in one place.

Here is why this matters for your practice:

- Automated reminders — clients who haven't submitted get automatic follow-up emails on a schedule you set. Your team stops writing "just checking in" emails, and clients actually follow through.

- Cloud storage sync — files land directly in Google Drive, OneDrive, SharePoint, or Dropbox, sorted into client folders. No downloading attachments, no dragging files into folders, no misfiled documents.

- No client account required — clients click a link and upload. No logins, no passwords, no "I forgot my username" calls from clients who just want to send you their tax return.

- Bank-level encryption — tax returns, account statements, and Social Security numbers stay protected with encryption in transit and at rest. You meet compliance expectations without adding friction.

- One submission for everything — questionnaire answers and documents arrive together. You open one submission and have the complete picture instead of piecing it together from six email threads.

The result: instead of a discovery meeting where you realize you're missing half the information, you walk in with complete data and spend the hour on strategy. For firms that manage ongoing client document collection, the same process works for annual reviews — send a fresh request with updated questions and the documents you need for the year.

Best Practices for Financial Planning Questionnaires

Send the questionnaire before the first meeting

Too many advisors still hand clients a paper form at the first appointment and watch them stare at question 12 trying to remember their mortgage rate. Send it digitally at least one week before the meeting with a clear deadline. Clients need time to look up account numbers, pull policy documents, and gather accurate figures. Rushing them in a conference room produces guesses, not data.

Explain why each question matters

Clients freeze up when asked for sensitive details without context. A brief note under each question changes everything — "We ask about your tax bracket to identify Roth conversion opportunities" or "Disability insurance is the most overlooked coverage for high earners." When clients understand the purpose, they complete the form instead of abandoning it.

Prioritize questions by planning impact

Not every question carries equal weight. Income, assets, debts, and retirement goals drive the plan. Put those high-impact questions first. If a client abandons the form halfway through, you still have what matters most.

Request documents alongside the questionnaire

Don't send the questionnaire in one email and follow up for documents in another. Combine everything into a single request. When clients upload documents at the same time they answer questions, you get complete information in one shot — and you stop spending your Monday mornings chasing attachments.

Update the questionnaire for annual reviews

Annual review questionnaires should be shorter and focused on what changed — new income, new debts, life events (marriage, divorce, new child, job change), updated goals, and accounts opened or closed. Some firms call this a pre-review questionnaire; whatever the label, keep it short. When you send the same structured request each year, clients learn the routine. By year two, most submit without a single reminder.

FAQ

How many questions should a financial planning questionnaire include?

Aim for 30 to 40 questions for an initial comprehensive plan. That covers personal information, income, assets, liabilities, insurance, retirement goals, risk tolerance, and estate planning without overwhelming the client. Most clients finish a well-organized questionnaire in 20 to 30 minutes when they have their documents handy. For annual reviews, trim to 10 to 15 questions focused on what changed.

When should I send the financial planning questionnaire to new clients?

At least one week before the first planning meeting. Clients need time to gather account statements, locate insurance policies, and look up balances. Include a clear deadline — "Please complete this by [date] so I can prepare for our meeting." Automated reminders at the halfway point and one day before the deadline make a measurable difference in completion rates.

What documents should I collect along with the questionnaire?

At minimum: federal and state tax returns (two years), statements for all investment and retirement accounts, mortgage statements, insurance declaration pages (life, disability, long-term care, homeowner's), Social Security statements, and estate planning documents (will, trust, power of attorney). For business owners, add business tax returns, operating agreements, and buy-sell agreements.

How do I get clients to actually complete the questionnaire?

Three things drive completion: make it easy, explain why each question matters, and follow up automatically. Use a digital form clients can open on any device — no PDFs to print, scan, and email back. Add context notes so clients understand each question's purpose. Set up automated reminders so incomplete forms don't sit in inboxes for weeks. And keep it focused — every unnecessary question reduces the chance a client finishes.

Should the questionnaire be different for married couples vs. individuals?

The core questions stay the same, but married couples need duplicate fields for income, employer benefits, retirement accounts, and insurance. Capture each spouse's risk tolerance separately — partners often have very different comfort levels with market volatility, and discovering that mid-plan creates problems. Add questions about joint vs. separate accounts and any prenuptial agreements.

Is a paper questionnaire or digital questionnaire better?

Digital wins on every metric that matters. Completion rates are higher because clients fill it out on their own time from any device. Data is legible — no deciphering handwriting. You can use conditional logic to show relevant questions based on previous answers. And a digital questionnaire can include file upload fields so clients submit supporting documents at the same time, cutting weeks of follow-up down to one submission. Choose a tool with encryption to protect the sensitive data you're collecting — your clients expect it, and your compliance team requires it.

Free Client Onboarding Checklist

Get the complete document checklist for your industry — interactive, with progress tracking.

Use the Free Checklist Tool →